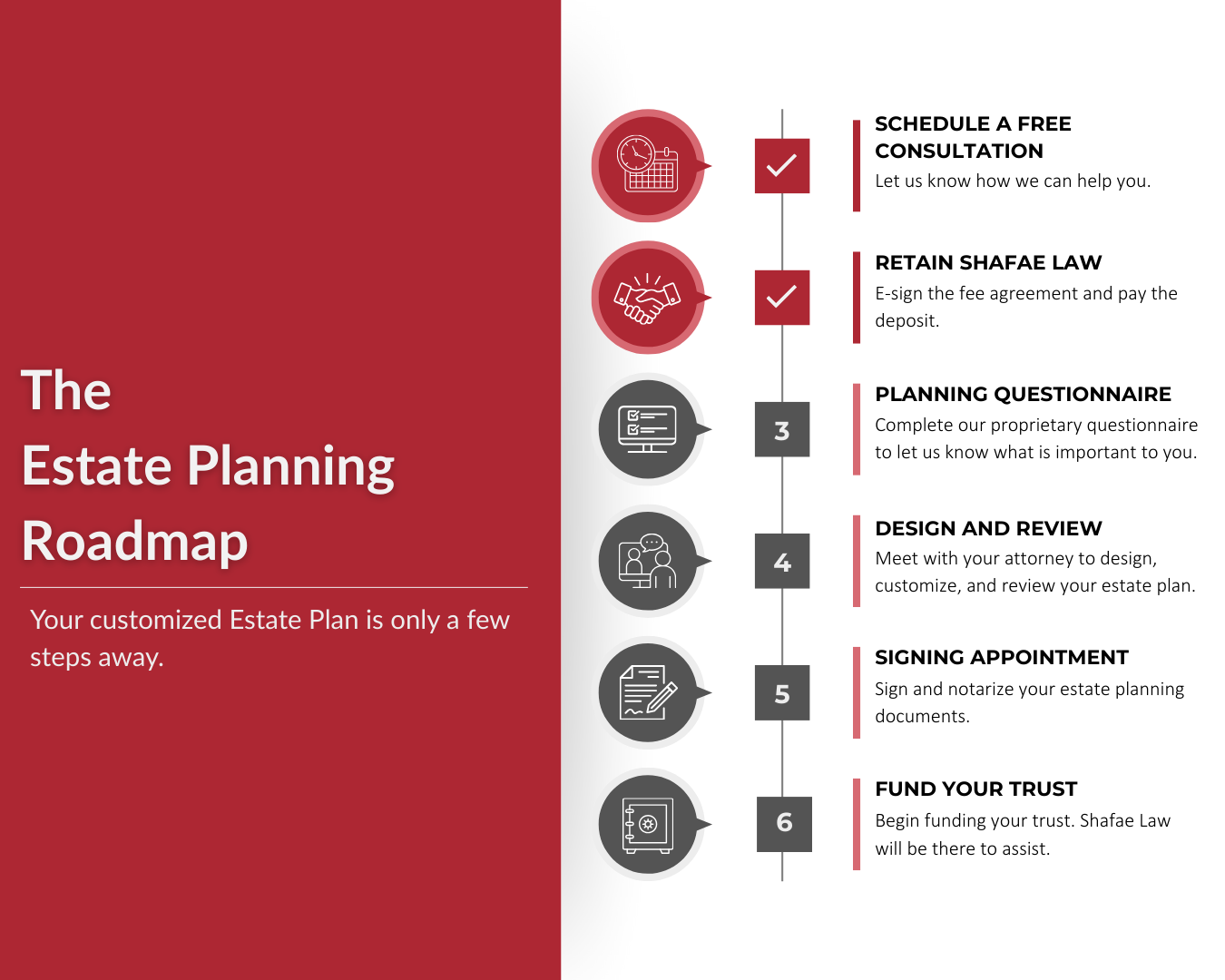

Welcome

Thank you for retaining Shafae Law for your estate planning needs. We look forward to working with you in the coming weeks. On this page, you will find helpful information to support you. Including:

A detailed breakdown of your estate planning tools

Tips to help you complete your Estate Planning Questionnaire

If you need additional support, please don’t hesitate to contact us.

Estate Planning Tools

Our comprehensive Estate Plan includes the tools listed below, the transfer of one California property into the trust (often, the family home) and all recording and notarization fees.

-

A California revocable living trust is a legal arrangement in which you transfer title to your assets into a trust you control during your lifetime, naming yourself as trustee and a successor trustee to step in when you die or become incapacitated.

Because the trust is revocable, you can amend or dissolve it at any time. At death, the assets pass under the trust’s terms without court-supervised probate, preserving privacy and reducing delay for beneficiaries.

-

A California pour-over will is a short testamentary document that “catches” any assets you forgot to title in your revocable living trust and directs (or “pours”) them into that trust at death.

It names an executor—often the same person as your successor trustee—and can handle guardianship nominations for minor children.

Because the pour-over transfer happens through the will, those leftover assets still pass through probate, so this document serves as a safety net rather than a replacement for proper trust funding.

-

A Durable Power of Attorney (DPOA) is a written authorization in which you, the “principal,” appoint someone you trust as “agent” or “attorney-in-fact” to handle financial and other non-medical matters on your behalf.

Unlike an ordinary power of attorney, it remains valid—or “durable”—even if you later become incapacitated, allowing the agent to pay bills, manage investments, file taxes, or sign legal documents without court involvement.

The principal can amend or revoke the DPOA any time while competent, and the agent must act in the principal’s best interest until the authority ends automatically at the principal’s death.

-

A California Advance Health-Care Directive (sometimes called a medical power of attorney plus living-will instructions) lets you appoint an agent to make treatment decisions and spell out your wishes—such as resuscitation limits or end-of-life care—if you become unable to communicate.

Estate Planning Questionnaire

Dedicate 45 minutes to complete and submit your questionnaire responses. This ensures that your Design Meeting is focused and productive. Below, we have detailed tips and best practices to help you complete each section.

-

Have everyone’s contact information handy. We ask for the contact information (name, address, telephone number, email address) of the persons you list in your estate planning documents.

Have access to your financial statements. We ask for general asset information (no balances required), bank account statements, brokerage and retirement accounts and any other asset information you plan to include in your estate planning documents.

Don’t let perfection hinder progress. Provide as much info as you can; we’ll discuss everything at your Design Meeting. Even incomplete information can be a helpful start to finalizing your decisions.

If you are married and completing a joint trust with your spouse, you only need to complete this questionnaire once. Plan to go through each section together and/or discuss important decisions ahead of time. The questionnaire will collect information about both spouse’s preferences.

-

You are asked to nominate three different types of Decision Makers. As much as possible, name at least one alternate for each role.

Legal Guardian for Minor Children: This is an adult that the court appoints (based on your nomination) to step into the parent’s shoes if both parents die or become incapacitated, handling the child’s day-to-day care, schooling, medical decisions, and overall welfare.

Choosing a guardian:

Prioritize shared values, emotional stability, and a strong, loving relationship with your child over factors like wealth or age.

Confirm the person’s willingness to serve.

Financial Decision Maker: This one person will cover three roles. These roles cover every phase of your financial estate planning needs:

The Successor trustee: assumes control of trust assets, manage investments, and distribute property when you die or become incapacitated.

The Executor (personal representative): gathers assets you inadvertently left out of your trust.

The Agent under a durable power of attorney: handles your financial and legal affairs during periods of incapacity without the need for court involvement.

Choosing a financial decision maker:

Trust and integrity: Pick someone who is scrupulously honest and can place your interests ahead of their own.

Financial competence: Choose a candidate who understands, is willing to learn, or is comfortable hiring a professional to help with basic investing, record-keeping, and tax obligations.

Availability and longevity: Opt for someone likely to be healthy, local (or tech-savvy), and willing to devote the time required to handle your financial affairs.

Low conflict potential: Avoid individuals whose relationships with your beneficiaries are strained. Consider co-fiduciaries or a neutral professional if family dynamics are complex.

Communication skills: Select a person who can explain decisions, keep records, and provide timely updates to heirs, advisors, and courts when necessary.

Medical Decision Maker: This is the person you authorize to speak with doctors and make treatment choices if you cannot communicate. Their authority springs from the document, remains effective during incapacity, and ends at your death, ensuring seamless consent for surgeries, medications, and end-of-life care without court intervention.

Choosing a medical decision maker:

Trust and shared values: Select someone who respects your health-care and end-of-life wishes, and understands your religious or cultural beliefs.

Availability and assertiveness: Select a person who is likely to be reachable in emergencies, can process medical information, and advocate on your behalf.

Emotional stability: Pick an individual who can stay calm, make rational decisions, and communicate clearly with both family members and physicians during stressful situations.

Proximity and familiarity with the medical system: Ideally, choose someone local—or tech-savvy enough for telehealth—who is comfortable asking questions to understand your medical options.

Name alternates and revisit often: Review your selections after major life events—marriage, divorce, relocation, or changes in relationships—to ensure your directive always reflects current realities.

-

If you’re married, you have two common schemes for your trust design:

Survivor’s Trust: This trust holds all of the assets after the first spouse in a joint revocable trust dies. The surviving spouse usually retains full control and ownership—can amend, add or withdraw assets, and remains the trustee—so the assets continue to avoid probate while remaining reachable for the survivor’s needs.

Because California treats community-property assets inside the Survivor’s Trust to receive a full step-up in income-tax basis at each spouse’s death, it also preserves valuable capital-gains benefits for heirs.

AB Trust: This is a joint revocable living trust designed for married couples that automatically splits into two sub-trusts at the first spouse’s death:

Trust A stays fully revocable and under the surviving spouse’s ownership and control.

Trust B (Bypass, Credit-Shelter, or Decedent’s Trust) becomes irrevocable, is funded with the deceased spouse’s share of everything, and its appreciation passes estate-tax-free to heirs when the second spouse dies.

Although today’s high federal estate tax exemption and portability rules make AB Trusts less common for tax purposes, they can still shield assets from a survivor’s remarriage or from the survivor’s creditors.

-

In the questionnaire, we provided the most commonly selected options. In the Glossary of Terms below, you can read more about each option. If you don’t see your circumstance reflected, feel free to add your preferences in the notes section.

Glossary of terms:

To our children, in equal shares, each getting their own trust for their own benefit: For minor children, each equal share is held in a trust to be managed by someone else, on their behalf, until each child reaches a certain age.

To our children, in equal shares, each receiving their share outright (not in a trust): For adult children who want the most direct, equal inheritance.

To our children, in one common pot trust: This keeps all trust assets in one “pot.” The trustee uses discretion to provide for all children simultaneously until the youngest child reaches a certain age.

To individuals who are not our children, in some proportion: This option allows you to provide for whoever you want.

To a charity or list of charities: This option allows you to contribute to causes important to you.

To a combination of individuals and charities: This option allows you to combine any of the above options.

Ultimate contingent beneficiaries: Referring to the backup plan in case ALL of your beneficiaries die before you. While unlikely, it’s important to consider and plan for all potential scenarios. For example, if your entire family perished in the same catastrophic event, who would be the contingent, or "back up", beneficiaries?This can be an individual ("Jane Doe"), a group of individuals ("Jane Doe, Roger Doe"), a class of individuals ("our cousins"), or a charity or other entity ("The SPCA")